Featured

Table of Contents

Integrating Financial Commitments in the Local Market

Managing a family spending plan in 2026 needs a high degree of precision as digital payment systems and subscription-based services have fragmented month-to-month costs. For numerous citizens in the local area, the challenge is no longer simply the total quantity owed, however the logistical complexity of tracking numerous due dates, rates of interest, and lender requirements. Professional debt management has moved far from high-interest private loans toward structured, nonprofit-led programs that focus on long-lasting fiscal health over short-lived liquidity.

Performance in 2026 revolves around the consolidation of numerous high-interest commitments into a single, manageable monthly payment. This procedure frequently involves working with a 501(c)(3) nonprofit credit therapy firm to work out with financial institutions. Unlike conventional debt consolidation loans that may just move debt from one account to another, these programs focus on decreasing rate of interest and removing late fees. Such a shift is particularly relevant in the current economic climate, where moving rates of interest have made charge card balances progressively hard to retire through minimum payments alone.

Economic data from early 2026 recommends that households using professional management plans see a significant enhancement in their credit profiles compared to those trying to handle multiple lenders individually. The structured nature of a Financial obligation Management Program (DMP) guarantees that payments are distributed properly throughout all getting involved accounts. This organized technique reduces the risk of missed due dates that frequently result in charge rates and credit score damage.

Consolidation Strategies for 2026 Spending plans

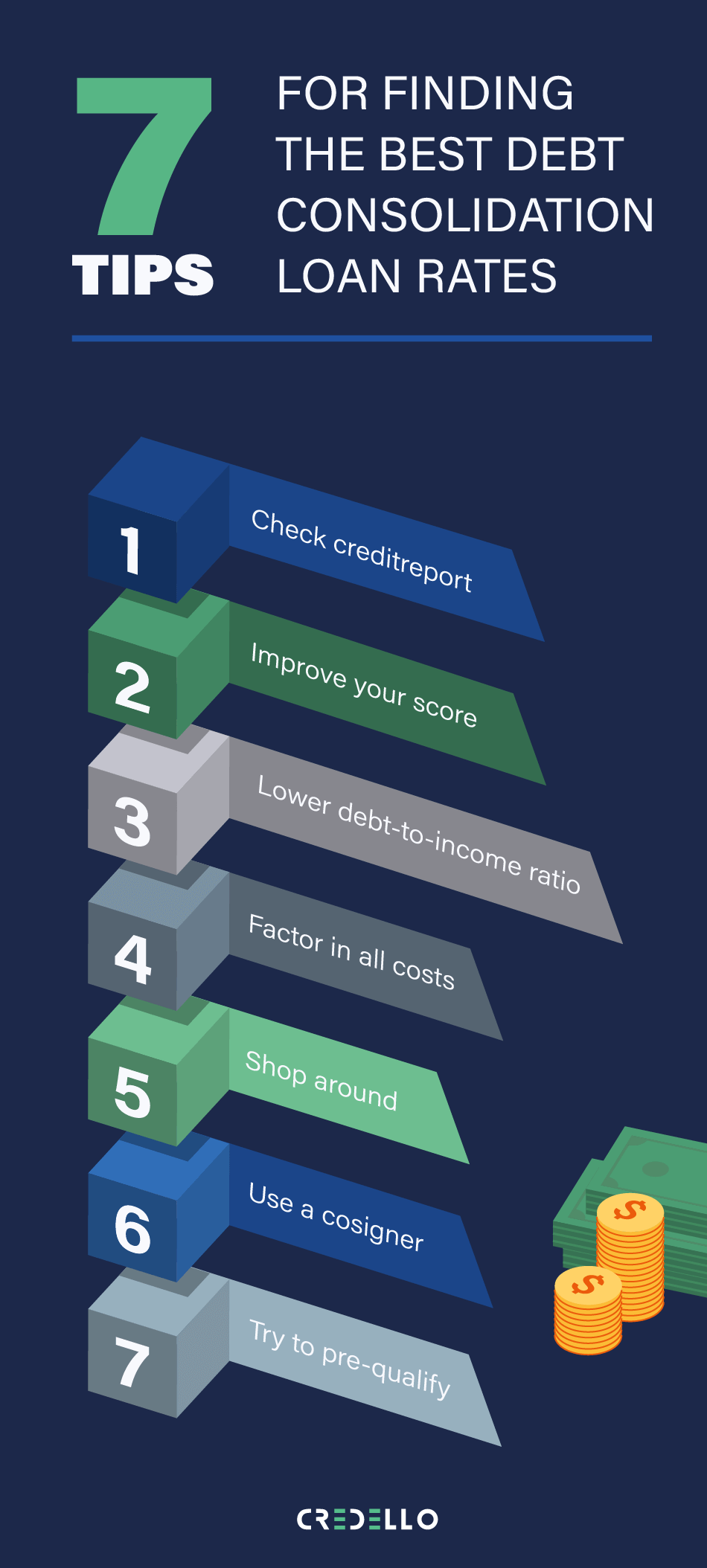

The distinction in between a personal debt consolidation loan and a not-for-profit management plan is significant for anybody seeking to stabilize their financial resources in the surrounding area. A combination loan is basically a new line of credit utilized to pay off existing ones. While this can streamline payments, it typically requires a high credit rating to protect a beneficial rate. In contrast, a DMP organized through a firm authorized by the U.S. Department of Justice does not depend on securing new debt. Instead, it counts on the agency's existing collaborations with banks to lower expenses on present balances.

Competence in Debt Management offers a clear advantage for individuals dealing with high-interest retail cards or unsecured individual loans. These programs are developed to be accessible to a broad variety of earnings levels throughout the United States. Due to the fact that the firms are nonprofits, their primary goal is the successful conclusion of the financial obligation repayment plan rather than the generation of earnings from interest spreads or origination costs. This positioning of interests is a hallmark of the 2026 financial services sector.

Digital tools have actually likewise changed how these strategies run. Many programs now incorporate straight with digital banking apps, supplying real-time tracking of how each payment lowers the primary balance. This openness helps keep the discipline needed to finish a multi-year plan. In the local market, community groups often partner with these companies to offer the needed local context, ensuring that the financial guidance represent local cost-of-living differences.

The Role of Nonprofit Assistance in Regional Finance

Not-for-profit credit counseling firms offer a suite of services that extend beyond simple financial obligation payment. In 2026, these organizations stay the standard for pre-bankruptcy therapy and pre-discharge debtor education. This regulatory oversight makes sure that the advice supplied satisfies rigorous federal requirements. For those in the region, this indicates getting a spending plan analysis that looks at the entire monetary picture, consisting of real estate costs and long-lasting cost savings goals.

Implementing Professional Debt Management Plans helps numerous families prevent the most drastic monetary steps, such as declaring insolvency. HUD-approved real estate therapy is frequently available through the very same firms, enabling an unified strategy that secures homeownership while attending to consumer debt. These firms operate nationwide, yet they maintain local connections through a network of independent affiliates. This structure allows a local in any state to get customized attention while gaining from the scale of a national nonprofit company.

Financial literacy stays a foundation of these programs. Instead of just fixing the immediate problem, counselors focus on teaching the underlying concepts of cash circulation management and credit usage. This instructional component is often delivered through co-branded partner programs with local companies or community colleges. By the time a participant finishes their management plan, they often have a deeper understanding of how to use credit properly in a digital-first economy.

Long-Term Benefits of Payment Streamlining

The primary objective of streamlining month-to-month payments is to reclaim control over one's discretionary earnings. When numerous high-interest accounts are active, a large portion of every dollar goes toward interest instead of principal. By working out these rates down-- often to no or near-zero percentages-- the repayment timeline is cut by years. This performance is what enables homes in the local vicinity to pivot from financial obligation payment to wealth building.

Individuals looking for Financial Relief in Dayton ought to look for agencies that use a clear fee structure and a history of successful financial institution negotiations. The 2026 market is full of for-profit debt settlement business that might guarantee quick outcomes but frequently leave the customer in a worse position due to high costs and aggressive strategies. The 501(c)(3) not-for-profit model stands apart by offering free preliminary counseling and capped regular monthly costs for those who pick to enter a management program.

Success in these programs is typically measured by the transition of the customer from a state of monetary stress to among stability. As the last payments are made, the counseling firm frequently assists with the next steps, such as reconstructing a credit score or developing an emergency fund. This holistic technique is why nonprofit debt management remains a preferred path for citizens throughout the country who are serious about their monetary future.

Performance in 2026 is not almost moving quicker; it is about moving smarter. By consolidating commitments into a single payment and benefiting from negotiated interest reductions, consumers can handle their debt without the weight of continuous collection calls or the fear of escalating balances. The procedure offers a structured, predictable path towards monetary self-reliance that appreciates the spending plan of the person while fulfilling the requirements of the financial institution.

{kind=link}

Latest Posts

Comprehending the Cycle of Financial Obligation in Local

How to Reduce Your Credit Card Interest Today

Navigating the Shift From High-Interest Cards to Debt Consolidation